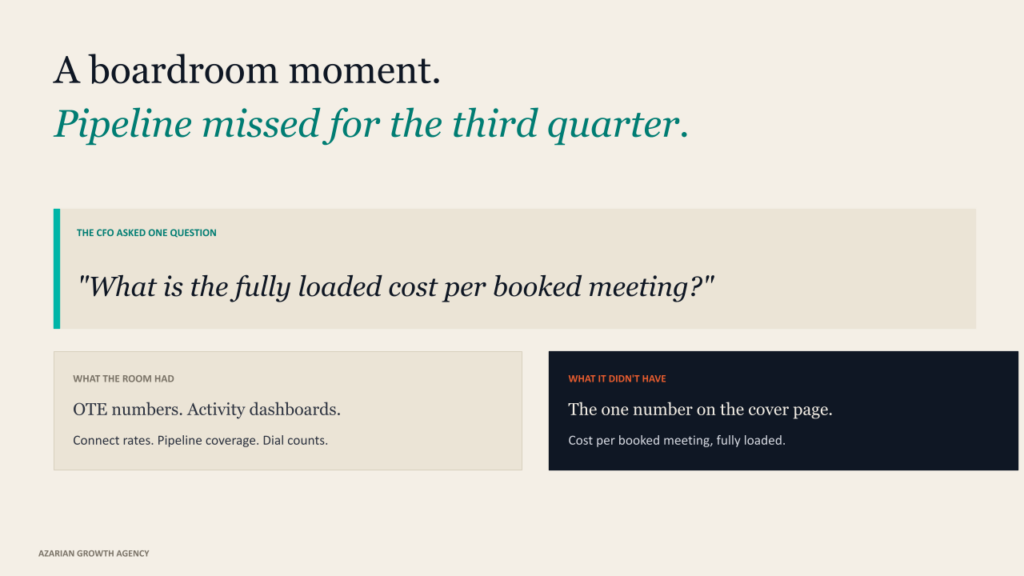

The first time I watched a CFO take apart an SDR org in real time was at a board meeting, maybe two years ago. The portco was missing pipeline plan for the third quarter in a row. The sales leader walked through the standard slides. Activity was up. Connect rates were holding. The team was hitting their dial counts. The CFO listened, asked one question, and then asked it again until the room got uncomfortable.

What is the fully loaded cost per booked meeting?

Nobody had a clean answer. Not the sales leader. Not the head of RevOps. Not the CFO. The room had numbers for OTE, numbers for pipeline coverage, and numbers for activity. It did not have the one number that should have been on the cover page. By the time we worked it out together later that week, the answer was uncomfortable, and the implication was worse. The SDR motion at that company was not just expensive. It was structurally broken in a way no amount of better coaching or better tooling was going to fix.

I have watched this play out at maybe a dozen portcos since. The conversation starts with the pipeline. It always ends in unit economics. And the unit economics on the SDR seat have shifted enough in the last 24 months that the model most companies are still operating on does not survive contact with a spreadsheet anymore. This post is the version of that conversation I wish I could just send people. Not an attack on SDRs. A rebuild of how the math actually works in 2026, what changed, and what an operator should do about it.

See the full agent system run live: the autonomous agents pipeline demo at Tech Week Boston.

The premise that does not survive scrutiny

The SDR role was priced when its work could not be done any other way. Researching contacts at scale, mapping buying committees, writing personalized outreach, monitoring trigger events, sequencing follow-ups. All of that required human eyes and human time, and the salary structure reflected that reality. A reasonable OTE for a competent SDR in a mid-market software company has held in the $75K to $90K range for years, and Bridge Group’s annual SDR compensation research has tracked the pattern long enough to be one of the better public benchmarks in the category.

The price was rational because the work was unambiguous. You needed humans. There was no other way to get the inputs that the rest of the funnel depended on.

The premise stopped being true sometime in 2024, and most companies have not yet repriced the seat against the new reality. The work the SDR was hired to do, almost all of it, can now be done by an autonomous pipeline system operating against a properly structured ICP and a verified contact graph. Not partly. Not as a copilot. The actual work, end-to-end, with the SDR removed from the research and list-building loop. We have written elsewhere about how to define an ICP that an agent can actually consume, which is the prerequisite for any of this to work, but the architecture itself is no longer experimental.

When the work moves and the price does not, the seat starts to function as a tax on the pipeline rather than a generator of it. That is the part most teams miss until someone runs the numbers carefully.

What an SDR seat actually costs

The headline number on the SDR seat is OTE. It is also the least useful number. The fully loaded cost of running an SDR program runs roughly two and a half to three times OTE once you account for everything attached to the seat. The math is not in dispute, just usually not added up.

Start with $80K OTE for a mid-market SDR. Add 25% to 30% in benefits and payroll taxes. Add manager overhead allocated proportionally per rep, since SDR teams typically run one manager per six to eight reps on a $140K to $180K OTE. Add the tool stack, which in 2026 includes a sales engagement platform like Outreach or Salesloft, a contact database like Apollo, an enrichment layer, a dialer, sometimes Clay or UserGems on top, and a CRM seat. Easily $400 to $800 per rep per month.

Then add ramp time. The honest median is three to four months before a rep is hitting full quota, which means the first four months of OTE produce a fraction of the pipeline the seat was budgeted for. Add the workspace cost. Add the lost pipeline from seats that are unfilled at any given moment, which, in a team of ten reps with industry attrition, is almost always one or two seats.

Add it up, and a single SDR seat in 2026 costs $200K to $260K a year fully loaded. ICONIQ’s State of Go-to-Market data has been one of the cleaner public sources on these patterns. Most operators arrive at the diagnostic with a mental number around $90K and walk out with a number closer to $230K.

The number is not what makes the model broken. The number divided by the actual output is.

The SDR seat does not cost what teams think it costs, and it does not produce what teams think it produces. The gap between those two numbers is where the model breaks.

The hidden line item nobody quantifies

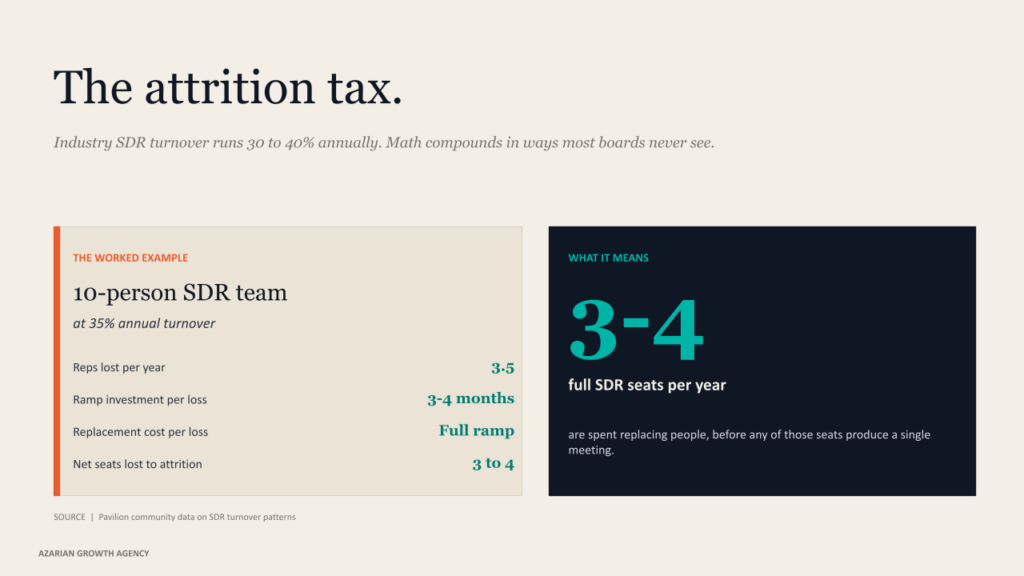

The fully loaded number above does not yet include the line item that actually breaks the math. SDR attrition. Industry-standard turnover on the role has hovered around 30% to 40% annually for the last decade, depending on which research you trust. Pavilion’s community data on this is one of the more honest sources because it pulls from operating teams rather than vendor surveys. Whatever the exact percentage at your company, the math compounds in ways most boards never see laid out.

Every SDR who leaves takes with them three to four months of ramp investment. The company paid for the ramp. The company gets none of the back half of the productive period. The replacement costs the same to recruit, the same to ramp, and produces the same fractional output for the first quarter. If you are running a ten-person SDR team with 35% annual turnover, you are spending the equivalent of three to four full SDR seats every year on the cost of replacing people, before any of those seats produce a single meeting.

When you fold the attrition tax into the fully loaded cost per meeting, the number that comes out is meaningfully larger than the number a finance team would calculate from base OTE alone. It is also remarkably stable across companies. The math works out to somewhere between $700 and $1,100 per booked meeting in most B2B mid-market software organizations, depending on motion shape, ICP fit, and tool stack maturity.

$700 to $1,100 per meeting is not the price of a meeting. It is the price of running an organizational structure that produces meetings as a byproduct.

What the agent stack actually replaces, and what it does not

Here is where I want to be careful, because this is the part of the argument that gets oversold by vendors and undersold by skeptics, and the truth lives in between. An autonomous pipeline system does not replace an SDR. It replaces the work an SDR does that is actually research, list building, enrichment, signal monitoring, committee mapping, first-touch drafting, and CRM hygiene. That is most of the SDR’s job by hour count. It is not all of it.

What it does not replace is the qualifying conversation, the discovery call, the late-stage objection handling, the relationship work that happens once a contact has actually engaged. Those still want a human. We have written separately about the autonomous agents vs. AI SDR tools distinction. The question is what mix of work belongs to humans and what mix belongs to agents now that the agent layer is real.

The substitution math gets interesting when you actually structure it. An autonomous pipeline system can run the research and outreach work for thousands of accounts in parallel. The cost per verified contact through Clay-style waterfall enrichment runs in the cents-to-dollars range. The cost per outreach touch generated by an agent against signal data is dramatically lower than the loaded SDR-time cost of the same touch. Jason Lemkin’s public reporting at SaaStr on AI SDR results landed in this neighborhood when the team published their honest write-up.

The work that survives, the conversation work, you want fewer humans doing more of. Three excellent reps having more high-quality conversations beats ten average reps doing more activity, every time, especially when the agent layer is feeding them better-qualified accounts than they could have surfaced themselves.

The breakeven question PE operators actually ask

When a PE operating partner sits down with a portco CFO to talk through this, the question that surfaces is rarely should we replace SDRs with agents. The question is, at what coverage level does each additional dollar produce more pipeline through the agent layer than through another SDR seat? That is a different question, and it has a cleaner answer.

The agent stack has a high fixed cost and a low marginal cost. You spend the first dollar building it. The thousandth account it processes costs almost nothing more than the hundredth. Once it is running, scaling coverage is mostly about ICP discipline and signal architecture, not about adding more compute. The SDR motion has the inverse curve. Each rep adds linear cost, linear capacity, and a fixed ramp tax. There is no economy of scale because the work is bound to human hours.

When you graph these against each other on a coverage axis, the breakeven shows up somewhere around 200 to 400 target accounts, depending on how complex your motion is. Below that, an SDR-only motion can be more cost-efficient because the agent infrastructure has not earned its fixed cost back. Above that, the agent stack pulls away decisively. By the time you are trying to cover a thousand accounts in your ICP, the SDR-only model is paying two to four times what an agent-augmented model pays for the same coverage, and the gap widens with every account you add.

This is the math that turns the conversation. The decision is not philosophical. It is operational. If your TAM is small enough that 200 to 400 accounts cover it, the SDR motion can survive. If your TAM is larger than that, which it is at most growth-stage and PE-backed companies, the agent stack is a fiduciary obligation, not a discretionary upgrade.

Where the math breaks down for agents

I want to give the honest counterargument here because the operators reading this are smart enough to make it themselves, and there is no point pretending otherwise.

The agent math breaks down in three specific places. The first is when the ICP is genuinely small. If you are selling a $2M ACV product to thirty enterprise accounts in the world, the agent stack is not the right architecture. You want senior humans doing concierge outbound to a curated list. The second is when the buying motion is dominated by relationship-based selling, which happens in some financial services, certain government contracting environments, and a few categories of high-touch enterprise. The third is when the ICP is poorly defined, in which case the agent will scale the wrong work faster than a human team would.

There is also a build-cost factor that operators should price in honestly. Standing up an agent system properly takes weeks of work from someone who can think in agent terms, and the GTM stack we run with Claude Code is not plug and play. Teams that try to retrofit agents on top of an existing CRM and an unstructured ICP usually produce a fragile system that costs more to maintain than the SDR seats it was supposed to replace. The build is real. The build is also a one-time cost, which is the main reason the math eventually wins for any team with a TAM above a few hundred accounts.

The honest version of the recommendation is that agent infrastructure is the right call for most growth-stage and PE-backed B2B companies in 2026, with the exceptions above. It is not the right call for everyone, and operators who pretend otherwise are selling something.

The diligence question PE and VC are actually asking

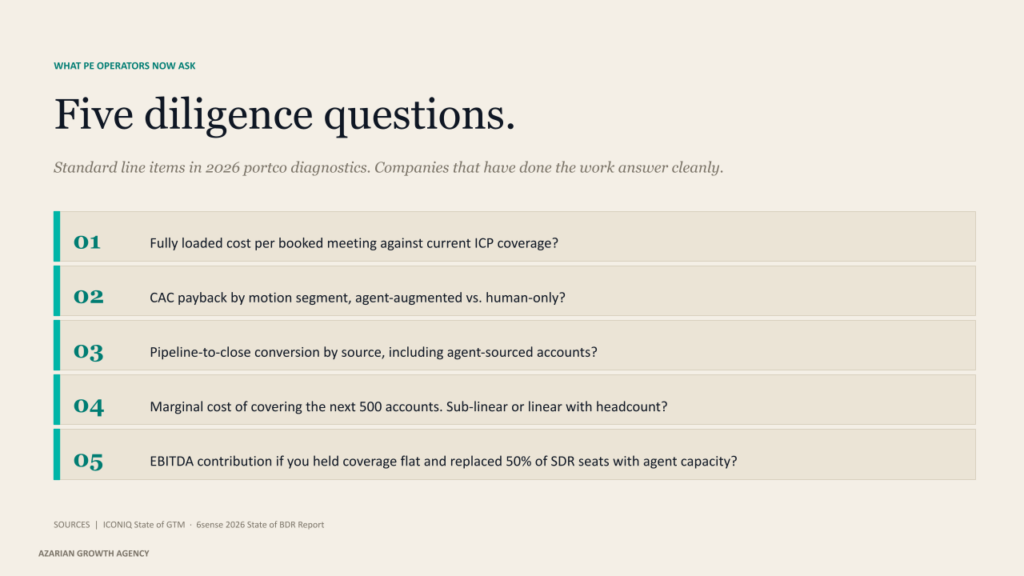

The reason this matters more in 2026 than it did in 2024 is that institutional capital has caught up to the math. 6sense’s 2026 State of BDR Report and the broader operator-grade research from ICONIQ’s GTM data have surfaced enough public benchmarks that the unit-economics question is now a standard line item in PE diligence. When an operating partner walks into a portco for the first time, the questions about the SDR motion are different from those they were two years ago.

The questions sound like this. What is your fully loaded cost per booked meeting against your current ICP coverage? What is your CAC payback by motion segment, separated cleanly between agent-augmented and human-only pipeline? What is your pipeline-to-close conversion by source, including the agent-sourced accounts? What is the marginal cost of covering the next 500 accounts in your ICP, and is that cost sub-linear or linear with respect to your headcount? What is the expected impact on EBITDA contribution if you held coverage flat and replaced 50% of your SDR seats with agent capacity over twelve months?

These are not gotcha questions. They are the questions a thoughtful operator asks because the answers determine whether the GTM motion is creating value or destroying it. Companies that have already done this work answer cleanly. Companies that have not are usually surprised by what surfaces when they try, and the surprise is rarely flattering.

What an operator should actually do

The honest playbook is simpler than it sounds. Run the diagnostic first, then make the structural call.

Start with the fully loaded math. Pull your real numbers, not your reported numbers. OTE plus benefits plus manager allocation plus tool stack plus ramp tax plus attrition tax. Divide by the actual booked meetings, qualified, not just dialed. Compare against the agent-stack equivalent at the same coverage level. The number gap will tell you what direction the change needs to go.

Then look at your ICP and your coverage. If your TAM is meaningfully larger than your current SDR team can cover, the case for an agent layer is straightforward. If your TAM is small and your ICP is tight, the case is weaker, and the right move might be to run a leaner human team with better tooling rather than rebuild around agents. The honest answer depends on the TAM math, not on philosophy.

Then look at your team. The reps you have are not interchangeable. The best of them are doing work that an agent cannot replicate well: the relationship work, the qualifying conversations, the late-stage problem-solving. The middle and lower performers are usually doing work that can move to the agent layer without revenue loss. The structural call is rarely to fire everyone or keep everyone. It is reshaping the org around the work that survives the transition.

And finally, build the agent layer if the math says to build it. Define the structured ICP before any agent gets wired up. Build the signal architecture that tells you which accounts deserve attention this quarter. Stand up the decision maker mapping layer so the agent ships verified contacts into the sequencer instead of guesses. The architecture compounds. Lean teams in particular benefit from this approach because one capable operator with the right infrastructure can produce more pipeline than five SDRs could on the old model.

The honest answer

If you are running a B2B outbound motion in 2026 and your CFO does not have a clean, fully loaded cost per booked meeting on a slide, that gap is the first thing to fix. It will not flatter the SDR program. It will probably not flatter whatever agent vendors you have already bought, either. It will tell you the truth about your unit economics, which is the only basis on which to make the structural call this work requires.

The SDR cost model is not broken because SDRs are not valuable. They are. It is broken because the price of the seat was set when the work could not be done any other way and most of that work now can. Companies that run the math honestly and rebuild the motion around the new reality will produce a better pipeline at a lower cost than companies that keep adding seats. The gap will compound, slowly at first, then quickly.

The teams that win this cycle are not the ones that fire their SDRs. They are the ones who figure out which work belongs to the agent layer, which work belongs to humans, and rebuild the cost structure to match. The math is not subtle once you do it. The hard part is doing it.

About Azarian Growth Agency

Azarian Growth Agency is an AI native growth marketing agency working with VC-backed founders, PE operating partners, and growth-stage B2B leadership teams. We build full funnel growth systems anchored on agent infrastructure, with 91 agents in production across client engagements as of 2026. Our work spans pipeline diagnostics, ICP architecture, decision maker mapping, intent signal infrastructure, and the broader stack of AI content marketing, AI-driven customer insights, and generative AI for marketing. The Strategic Growth Diagnostic is the entry point for most engagements: a structured assessment of pipeline, CAC, signal infrastructure, and agent readiness, framed against the metrics PE and VC institutional buyers actually use.

I run a recurring live demo of the autonomous agent system that the agency builds for B2B clients. The session walks through the full agent handoff in real time. The TAM and signal scoring agent. The Decision Maker Finder. The persona and outreach agent. Attendees see the prompts, the data flows, the verification checkpoints, and the metrics framework that ties the motion back to the pipeline and CAC payback. The session is built for VC-backed founders, VPs of Sales, and operating partners evaluating GTM efficiency at the portfolio level.

Check the webinar: Tech Week Boston autonomous agents pipeline session.